Underfunded pensions have become an increasingly important issue in public finance in recent years. In this policy area, CALDER research has focused on the systemic underfunding of state educator pension plans. CALDER Working Paper 148 documents and explains "Unfunded Actuarial Accrued Liabilities" (UAALs) in state plans. UAALs are transfer payments used to cover the cost or liabilities – effectively debt – owing to previous plan operations. The shortfall is caused by a variety of factors across states, including retroactively implemented formula enhancements, unmet actuarial assumptions that have resulted in perpetual funding shortfalls, and government agencies underpaying - or not paying at all - required contributions on the behalf of teachers. The end result in a substantial financial burden on the current system, which must pay what a "pension tax" to cover these previously-accrued liabilities.

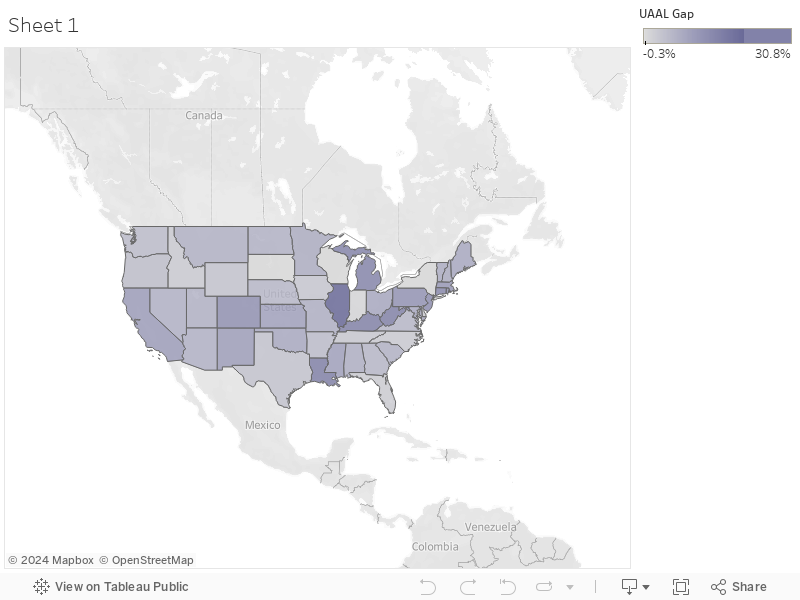

The following map uses data from CALDER Working Paper 148 to identify the contribution gap in defined benefit state educator pension plans, based on 2013 reports. The gap is calculated by subtracting the “normal cost” (i.e., the actuarially estimated funding needed to provide promised pension benefits for currently working teachers) from the actuarially required contribution rate. The contribution gap is essentially the amount of current spending that goes towards meeting UAAL payments.

The average gap across 49 states (excluding Alaska) is 10.89% of teacher salaries. This amounts to a large reduction in real operating spending per student and makes clear that a significant fraction of the resources allocated toward teacher compensation are not being invested in resources to educate today's students at all.

Contribution Gaps in Defined Benefit Pension Plans (2013)

Note: Alaska is excluded from the map because the defined benefit pension plan was closed as of 2013.

Clarity of Documentation Key: "High" means the data taken directly from a plan report and presented in a very straightforward way; "Medium" means data are from report but note the report is not perfectly clear; "Low" means reports are not clear and/or unavailable for the timespan needed. In these cases we pulled data from the Public Plans Database maintained by the Center for Retirement Research at Boston College.

In cases of "Medium" or "Low" data clarity where subjective decisions needed to be made, we made a decision that goes against finding high UAAL costs.

More details about how we arrived at the gap numbers for individual states are available upon request. Please contact CALDER using the “Contact Us” tab.